Using MacroRisk Analytics software, this post will present the betas, up-market betas and down-market betas for 10 stocks out of the S&P 500 Index with positive returns year to date (through 6/10/19) that have the highest and lowest return-to-risk ratios from 12/31/18 through 6/10/19. We first discussed these stocks in another blog post which you can check out by clicking here.

As a reminder, beta measures an asset’s systematic risk or the risk of an asset relative to a benchmark over a certain period of time. It measures systematic risk, attributed to the market movements (e.g., the S&P 500 Index). It doesn’t include unsystematic risk which is the portion of total risk that is not explained by the market (e.g., company-specific information). Suppose a stock has a beta of 1.20. This means that over the time period during which this beta statistic was calculated, the stock was 20% more volatile (i.e., riskier) than the benchmark. Suppose the benchmark went up by 1%, a stock with a 1.20 beta would go up by 1.2% and vice versa. If an asset has a beta that is higher than one, it is riskier than the benchmark and while a beta of less than one would indicate the asset is less risky than the benchmark.

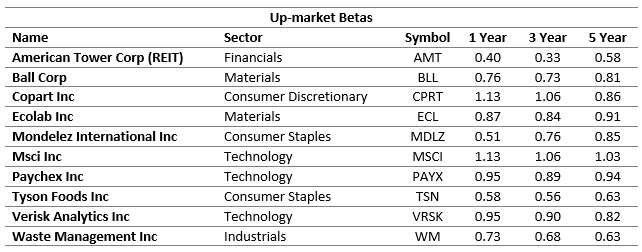

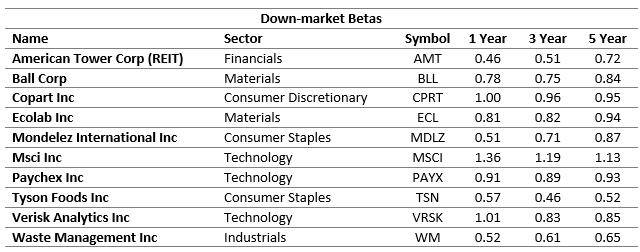

In addition to showing the regular betas, MacroRisk Analytics software provides up-market and down-market betas. Up-market betas are calculated using returns information for days when the benchmark returns are positive, and down-market betas are calculated using returns information for days when the benchmark returns are negative. Up-market betas measure how much more volatile an asset is when the benchmark goes up. If an asset has a up-market beta higher than 1, the stock would be expected to have higher returns than the benchmark when the benchmark goes up and vice versa. In this case, the up-market beta (i.e., up-market risk) is the good kind of “risk” or the “risk” of earning more or less money relative to the benchmark when the benchmark goes up. The down-market beta, on the other hand, measures the downside risk. What happens to the stock when the benchmark goes down? If an asset has a down-market beta of less than 1, it tends to lose less value on average than the benchmark when the benchmark goes down and vice versa.

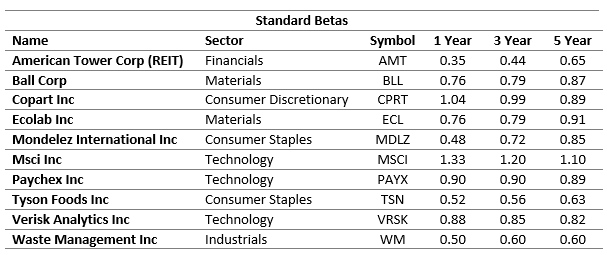

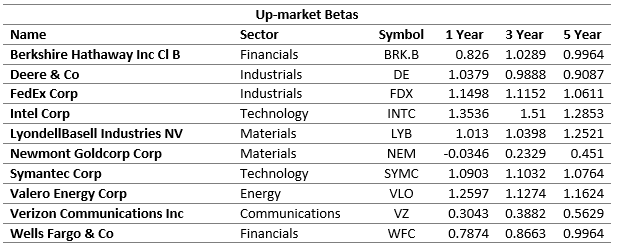

Now, let’s dive into the betas, up-market betas and down-market betas for our stocks. Using the Beta+ Holdings Table provided by MacroRisk Analytics, not only can we quickly get this information, but we can also customize the benchmark (e.g., an index, a ticker, or a previously created portfolio), the period over which we want to calculate the betas for and the frequency of returns. We used the MacroRisk Beta+ Holdings Table to export the beta results using 1, 3, and 5 years of daily returns with the S&P 500 Index as the benchmark to an Excel spreadsheet. The results are summarized below for 10 stocks out of the S&P 500 Index with the highest return-to-risk ratios from 12/31/18 through 6/10/19:

Next, we want to highlight which up-market betas were higher than their corresponding down-market betas. These are the situations when the stock has increased more than the benchmark when the benchmark went up and lost less value than the benchmark when the benchmark went down. We indicate these occurrences with a ‘1’ in the table below:

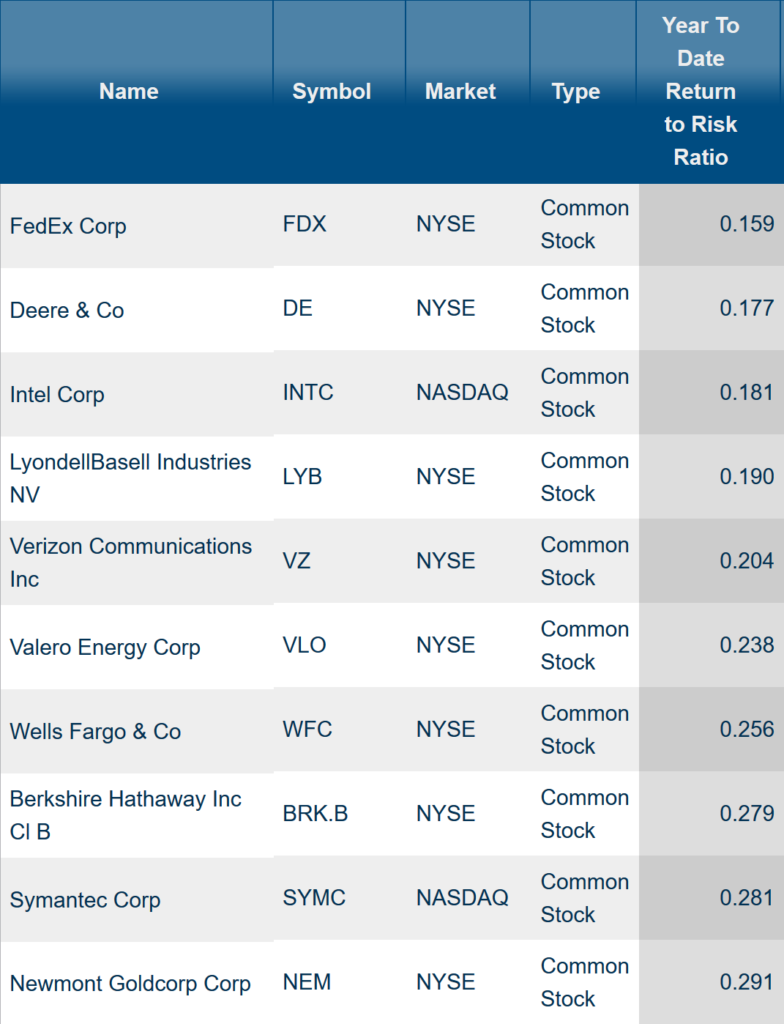

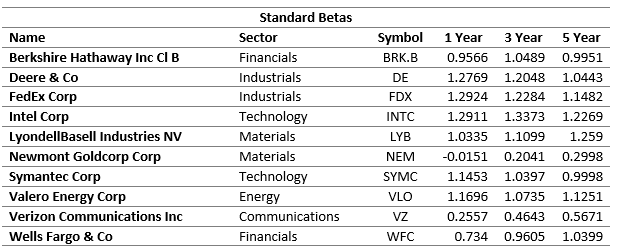

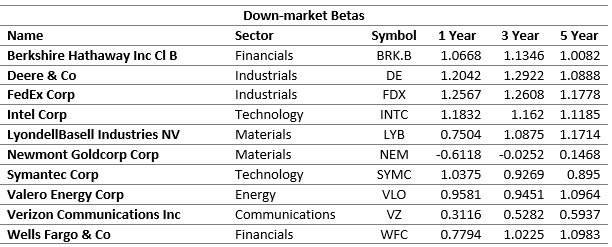

Shown below are the betas, up-market betas and down-market betas for the 10 stocks from the S&P 500 Index with positive returns that have the lowest return-to-risk ratios from 12/31/18 through 6/10/19.

Lastly, we identify which of these stocks had higher up-market betas than down-market betas.

Using these tools, we have presented the betas, up-market betas and down-market betas which can help investors get a better understanding of how the assets have performed relative to the S&P 500 Index, our selected benchmark.

MacroRisk Analytics has a selection of proprietary analysis tools that use macroeconomic variables to provide information on tens of thousands of stocks, mutual funds, exchange traded funds, and other traded assets. Click here to see how MacroRisk Analytics can help you.